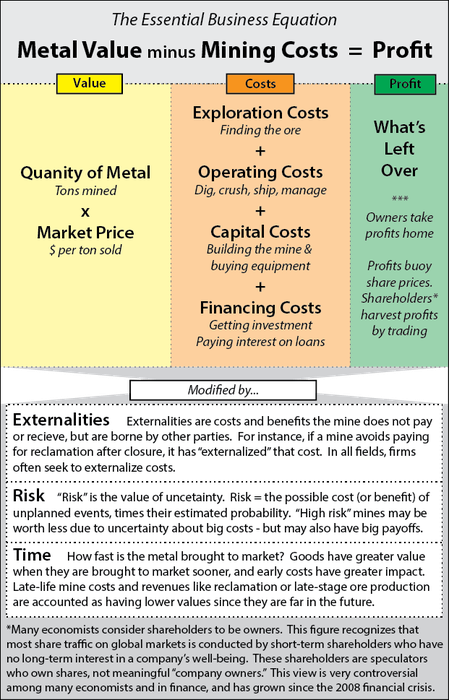

Metal Mining Business Equation

Mines are businesses just like any other, and must have revenues that are larger than their expenses, to be profitable.

Exploration: "Exploration" isn't a separate cost category that most accountants recognize, but to illuminate how mines work economically, we treat it here as being separate from operating, capital, and finance costs.

Exploration is an extremely "risky" costs, since it might discover that an ore body is extremely valuable, but is more likely to discover that it isn't worth mining at all. For every prospect which is eventually mined, many prospects are abandoned after exploration, sometimes after tens or hundreds of millions of dollars in exploration costs. For example, in 2013 international mining firm Anglo-American wrote off more than $500 million dollars in Pebble Mine exploration, and the global giant Rio Tinto subsequently abandoned its entire ownership stake in the firm which holds the Pebble claims.

Start-Up Costs: When a mine proceeds beyond exploration and into operations, it requires a big start-up investment in construction and equipment. The mine pays this money back over many years. Financing costs are essentially the "cost of renting that money."

Profitable or Not? A mine may be called "unprofitable" until has generated lifetime revenues greater than its lifetime debts and costs. From a long-term business perspective, this is an accurate statement. However, a mine can generate a strong cash flow long before it is officially profitable, making money for its owners and managers. For example, a simplifed hypothetical mine might have these characteristics:

$100 million borrowed for exploration & mine construction The mine is $100 in debt as operations start.

$10 million in loan interest payments (financing cost) in its first year of operations.

$25 million in operating costs, the first year.

$40 million of metal produced and sold, the first year.

$3 million payment on the $100 million financing, the first year.

In this scenario, the mine has $40 million in revenues and $38 million in costs in the first year of operations. The owners take home $2 million in cash. From a "personal" perspective, the enterprise is doing well: it generates a strong cash flow.

From an accounting perspective, however, the mine is "unprofitable" and will be so for many years, beause the total revenues are less than the total lifetime costs and debt. The mine needs to pay off its initial financing, and it will only be truly profitable once that's done.

This can get much more complicated, using perfectly legitimated accounting. For instance, if owners are employed as managers and draw salaries, then they can write of their own compensation as a cost, reducing the net income of the mine. If any "creative" or manipulative accounting is used, the real situation becomes vastly more obscured.

These practices aren't special to mines. People may describe any business as "profitable" or "unprofitable" for public relations or persuasive reasons, rather than to convey the economic reallity of the situation. They may also describe a business's finances in confusing or marginally accurate ways, because the actual situation isn't understood by a layperson without a business background - or because the true status of the business is viewed as a trade secret.

Cutting through the Confusion:

A good rule-of-thumb to cut through confusing messaging (or unfamiliar accounting lingo):

1. A business can only continue to operate if the long-term cash flow is positive.

2. A business withers and dies if it has negative long-term cash flow.

3. It often makes sense to continue operating many businesses with big debts, even with debts that will never be paid off, as long as the cash flow is good and the financing costs aren't overwhelming the business's ability to pay its employees, managers, and owners.

3. A business with negative cash flow can only be kept alive by constant infusions of outside money (such as fresh loans, investment, or subsidies) or by spending down a massive stockpile of money.