Coal Taxes, Rents, and Royalties in Alaska

Last modified: 12th August 2019

Summary

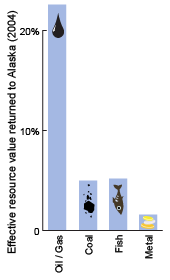

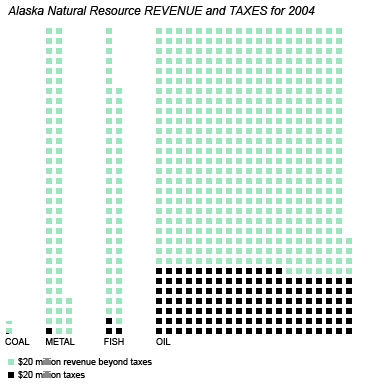

Mining in Alaska, including coal mining, returns a far smaller percentage of revenue to the state as taxes, royalties and rents than does the oil and gas industry. While the oil and gas industry pays around 20% of total revenue (still the lowest in the world), coal mining pays only 5% and metals mining less than 2%. All extractive industries in Alaska receive subsidies from the state including roads, infrastructure, cheap land and tax breaks. These public investments have led some people to question whether mining taxes and royalties should be more in line with what the oil and gas industry pays.

Variable state tax rates

The State of Alaska calculates the tax that it levies on different natural resource industries in dramatically different ways. In addition to statewide resource taxes, mining companies pay mineral rents and royalties to the state, a corporate income tax, municipal and borough taxes, conservation surcharges, as well as other levies.

These numbers are further modified by various deductions and exemptions, meaning that the amount a company actually pays might be very different from the nominal rate. A comparison of the tax rates levied by Alaska on the hard rock mining industry and the oil and gas industry is discussed in detail in our companion article “Mining Taxes and Revenue in Alaska”.

Coal in Alaska

Coal mining provides direct revenue to the state in the forms of taxes, rents, and royalties. In Alaska these are currently set as follows:

Rent: $3/acre/year

Royalties: 5% of Adjusted Gross Value (defined as price minus transportation costs)

Mining License Tax: $4,000 plus 7% net income (If net income is over $100,000)

(Additional Notes: There is a 3.5 year mining license tax exemption for new mines. State income tax is deductible from the mining license tax. Alaska allows 10% depletion against gross income. The rents on coal leases can be credited against royalties.)

Based on published numbers for rents and royalties and our calculations of the mining license tax, we estimate that the coal industry in Alaska pays around 5% of the value of the coal (see Sidebar). As shown in Figure 1, this is more than metals mining but much less than the amount paid by the oil and gas industry.

The debate

Proponents of Alaska’s existing tax regime for mining argue that having low taxes and fees results in increased investment by mining companies, leading to economic growth and increased employment in the state. The recent ranking of Alaska as the #1 U.S. state for mineral investment by the 2011-2012 Fraser Institute survey of mining companies supports this perspective.

However, coal mining in Alaska is a relatively minor employer. The industry employs only around 500 people, either directly in mining itself or indirectly in the use of the coal for the generation of power. Relatively little revenue from these activities is contributed to the state, and the mining activity is associated with a host of negative environmental and externalized economic impacts. Furthermore, only half of the coal mined in Alaska is used for in-state electricity production, the rest is exported overseas.

Estimating coal taxes:

_

Assuming a very high profit margin of 25% (just above the 2011 average of top 40 global mining companies) and no deduction of state income tax (unlikely) we can estimate that the mining license tax on Alaskan coal in 2010 was up to $1,281,500, which combined with the known $2,378,860 in rents and royalties equals $3,660,360 or about 5% of the $73 million market value of the 2,061,000 tons of coal mined that year.

We can also calculate the taxes, rents, and royalties paid by a hypothetical company using just the published rates and various known deductions. This gave us an estimate of 5.5% of the total resource value paid to the state.

_

This discussion typically revolves around the “best interest” clause of the state constitution:

“It is the policy of the State to encourage the settlement of its land and the development of its resources by making them available for maximum use consistent with the public interest” … “The legislature shall provide for the utilization, development, and conservation of all natural resources belonging to the State, including land and waters, for the maximum benefit of its people.”

Proponents of the current tax structure argue that the increased investment, economic activity, and domestic energy production facilitated by low coal taxes are in the maximum public interest. Opponents counter that the true cost of coalnegates these economic impacts, and that coal mining and combustion have unacceptable environmental and social impacts. The cost-benefit analysis of low coal mining taxes is further skewed if the coal is mined by non-Alaskan corporations and exported overseas.

Proposed changes

There have been several legislative efforts to change the mining tax structure in Alaska in recent years, for example with HB 40. This bill, proposed in 2009, would have made numerous changes in the way coal is taxed in the state. By our calculations this would have raised the amount paid by an established coal mining company from around 5% to around 7%, with all of that change coming from an increase in the mining tax. The increase would have been greater for new companies since they would no longer have gotten a 3.5 year exemption from the mining license tax, they would instead have received a deferral, payable over 10 years. Other versions of this bill, covering both hardrock and coal mining have since been proposed (e.g. HB 58).

Further Reading

Created: Jan. 19, 2018